We are still in the middle of the reboot which is reshaping the whole media business. At the time of writing, in mid-September, the nation is also still grappling with a number of wobbly health and economic variables, all of which will impact on how we do business. Everything feels a bit provisional and “in limbo”. Yet our businesses do not stop and have to churn on.

As for the new 2020 mediafutures international, at the time of writing, we are still in the active fieldwork for the international sample. Yet the UK segment has just been completed and closed off, so we can get an early read of what is happening here in our own domestic market.

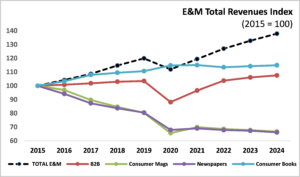

Yet before we dig into the survey detail, let us take a quick look at the broader UK entertainment and media market. The graph shows the trend in industry revenues tracked by the latest PwC Global Entertainment & Media Outlook 2020-2024.

- The Total E&M market was powering along at an average annual growth rate of +5% before the pandemic hit. It is predicted to dip by -7% in 2020, before returning to +5% per year growth rates from next year on, driven by hot segments such as VR, OTT Video and Video Games & Esports.

- An intriguing benchmark category is Consumer Books which is actually predicted to see accelerated growth in 2020 (+4%) before flattening out through to 2024. But that is another story for another time…..

- B2B was showing modest +1% annual growth before the 2020 collapse in advertising, live events and legacy print products, which all combined to create a -15% 2020 drop. After a strong 2021 and 2022, the sector is forecast to plateau through to 2024.

- Consumer Magazines and Newspapers, including all their print and digital platforms, show broadly similar trends to each other. Both were steadily declining by -5% per year up to 2019, both saw big falls in 2020 (-18% and -16% respectively). The PwC view is that neither segment will claw back their 2020 losses, but will emerge into 2021 with a smaller, but more stable and efficient businesses.

Moving to the sharp end of the companies reporting into mediafutures and the picture is much more of a rollercoaster and much more varied and complex from company to company, as the full report, available in October, will show.

Take a simple, but important leading indicator of change: staff headcount. Here, the 177 UK companies who reported in this year’s survey show the following topline figures:

- The minority (16%) are increasing their headcount. These companies tend to split into two groups. Either they have just bought out another company or their assets, or they have already gone through the pain of restructuring and are beginning to staff up – often with people with very different skills and experience to those already there.

- The biggest group (47%) have steady staff numbers. Again, these companies split into two groups: those who are still dithering about making permanent workforce changes after temporary furloughing and those who have already stabilised their businesses.

- A significant 37% are still into cuts with a reducing

Setting reducers (37%) against increasers (16%) produces a negative “net score” of -21%. So, the industry is still shrinking in staff numbers at a significant rate. Predictably, the negative net scores are highest by far in Events / Conferences / Exhibitions (-53%). Then comes Customer Publishing (-42%) and News Media (-37%). There is then a big gap before B2B (-20%) and Consumer Media (-17%) where staff numbers are reducing at their slowest rate.

So, the overall picture is that the industry is still in the middle of a fundamental business reboot, but that a number of companies are coming out the other side with teams of people who are ready for whatever opportunities or challenges emerge.

Behind the simple headcount numbers lie all kinds of complex issues related to company culture & organisation, as well as staff skills, experience & attitudes. That is why a number of key industry players, large and small, are saying that “staff” are both their biggest asset and their largest barrier to change at the same time. One of the most progressive Consumer Media companies sums it up like this…. “We have an open staff culture where staff are encouraged to take their own risks and try out new ideas. Yet getting the right staff right across the company, who are comfortable working in a fast-moving organisation, which is experiencing major and constant change – that remains an ongoing challenge for us.”

And then add in another complexity, which is now baked into the new-look media company: WFH (Working From Home). Put to one side the obvious savings in office overheads and the fact that many people are working more effectively and efficiently as a result, there appears to be a growing concern that something is being lost in the endless stream of Zoom meetings. As another industry-leading media company puts it…. “Remote working has undoubtedly reduced the overall sense of corporate community and common purpose. At a time when we need to work faster, more creatively and collaboratively than we ever have done before, that is a major missing. We somehow need to find a balance of working practices that make more sense than what we currently have.”

In future articles, we shall dig into all the key metrics tracked by mediafutures, such as turnover and profitability trends; digital “to do” lists; subscription opportunities and what to do with the newsstand; what people are spending on marketing, NPD and tech investments; and much more! We shall also have data from the new international dimension of the project with companies in Europe, Asia Pacific and the USA already engaged.

Back to news